If I said to you “I’ll show you how to prepare a cash flow forecast in under 30 minutes” would you believe me?

If you have spent half a lifetime in spreadsheets, you may well be sceptical as that’s never simple. Possibly adding new rows, tweaking formulas, double-checking the numbers as you review the forecast each month. Love it or hate it, a business needs a good cash flow forecast. This article published in Smart Company has some good tips on how to approach it.

Today, I will share with you my thoughts on how to prepare a fast cash flow forecast in under 30 minutes using Calxa. Yes, the budgets may not be perfect or final. However, they will be ready to develop and adjust over time as you contemplate your future plans. You will have a structure to build on and each time you repeat this process, the less time you’ll need.

What I want to demonstrate to you is that if you have all the information, there are tools out there that help you prepare a cash flow forecast with less fuss and effort. A forecast that will give you a view of your future cash position. One that will guide your business and you to make informed decisions.

Initial Preparation before Preparing a Forecast in 30 Minutes

The secret to efficient creation of a fast cash flow forecast is good, solid preparation. If that’s done well, the forecast is often simple to do. Of course, there are exceptions where the business is really complicated but even then, a rough draft can be better than having nothing at all.

Keep your Accounting System in Good Shape

Having the accounting system in good shape means you have a good starting point for your forecasts. It also gives you reliable numbers for the past periods. From here, you can build next year’s budget.

We suggest you use our Foundations of a Great Cash Flow Forecast checklist. Completing this worksheet will give you much of the information you need to prepare the forecast. What’s more, it will highlight any areas that might need fixing up first. The worksheet will make sure your accounting system is in good order with the bank, debtors and creditors reconciled. Without these fundamental accounts being correct, it’s impossible to have a good starting point for your forecast.

If you are not able to reconcile these accounts, talk to your accountant or bookkeeper, quickly! With most of us using some sort of cloud accounting these days, there is little excuse for not being up to date.

Other Information

In addition, the worksheet will guide you to preparing the information you need on current loans. This includes arrangements to pay outstanding tax liabilities. A cash flow forecast without balance sheet movements included is of little use to anyone. Fortunately, Calxa handles the more complex accounts like GST/VAT, Debtor, Creditors and Bank. The accounts you need to deal with are mainly:

- Loan repayments,

- Asset purchases

- And, new loans to finance those capital purchases.

If you use the checklist to prepare for your meeting with your advisor, it will give them an idea of your plans for the next year or longer. Ideally, you will specify how much profit you want to make and how you plan to achieve that. Your advisor might be wise to question your assumptions and the practicality of your plans, but that’s what they need to do to help you. They will review and critique the assumptions and help you come up with something that is workable and achievable.

The worksheet will also outline your planned capital purchases and how you plan to fund them so that you can incorporate these into the budget.

Time Challenge Starts (remember my claim of ‘how to prepare a cash flow forecast in under 30 minutes’)

How to Prepare a Forecast in 30 Minutes

Create and Update a Budget

After connecting to your accounting system, the next step is to create a budget for both the Profit & Loss and Balance Sheet accounts.

I use the Budget Factory in Calxa to produce the first draft of the P&L budget. This can be driven from an increase over the previous year or by setting a target profit figure. To set the profit target, you simply switch the Cost of Sales accounts from being an increase over the source year to being a percentage of sales. This makes the profit line editable, and the income is then calculated to show what needs to be earned to achieve that profit.

As always, this is an important moment to have that discussion with your advisor on how achievable that income change is. You don’t want to shatter your own dreams and ambitions but you do want to make sure you are going in the right direction to be able to achieve your goals.

The next step is to adjust the budget based on the worksheet. The emphasis here is on the balance sheet items. Make sure you’ve included all the planned asset purchases, as well as the new and existing loans. Use the loan wizard to add the loans. As long as you have the loan amount, start date and term, you can then choose to use either the interest rate or the monthly repayment amount. Our article How to Budget for a Business Loan will give you some tips on using this useful tool.

For the income and expense accounts, the focus is adjusting what’s different from the previous years. Have a look at our Budget Editing Tips for some quick ways you can update totals and use formulas to speed your budgeting. Start with the bigger line items first and leave the smaller ones to review later once you have the big picture established.

Time Check: 17 minutes

Review the Cashflow Settings

Timing is at the heart of a cashflow forecast. The important part is predicting when cash is paid or received.

Firstly, I check that the GST/VAT, Wages, and basic cashflow settings are right. Consider any changes in supplier and customer arrangements that may have been made recently. These settings will make sure you make a good estimate of the timing of payments and receipt.

For the Wages, enter the average amount of tax you withhold from wages to split the budget between net pay that goes out every month and the tax that is paid later. Run a payroll report for 12 months or so and divide the tax by the gross wages to get a sensible number for your business.

While Calxa provides the ability (in the Advanced Cashflow Settings) to adjust timing on an account-by-account basis, this isn’t necessary for most small businesses. Even when it is needed, it’s generally on a small number of accounts. The standard cashflow settings create a profile based on the average debtor days and creditor days in the accounting system. This is updated every time there is a sync so it’s always using current data. Review the forecast for reasonableness before spending time fine-tuning too much. You may not need much adjustment. Save the manual settings for those accounts that will make a material difference to your cashflow.

Time Check: 22 minutes

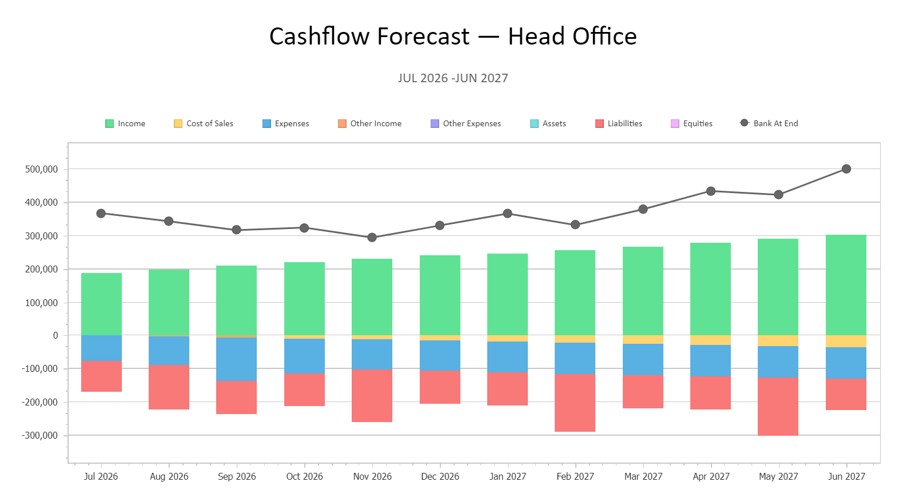

Prepare Reports

Now to the best part. I use the 3-way Forecast Report Bundle to produce a set of reports. This bundle includes the full cashflow forecast, balance sheet forecast and Profit & Loss Forecast. If you are finding the number reports overwhelming, you could exclude some reports and focus on the charts. Tailor the bundle so it gives you enough information to make decisions but without overdoing the detail. When you create the bundle, you have the option to choose not just which budget to use but also an Account Tree.

Use this to configure the reports to provide a more summarised version if there is too much detail with all accounts shown.

If you are preparing the forecast for your bank, add a cover page with your logo using the document editor. This will ensure the reports are professional and recognisable as coming from you.

Time Check: 25 minutes

The Final Step to Forecast in 30 Minutes

So, my last step in this process is to prepare a cup of coffee and review my cash flow forecast.

Not bad right? I prepared a fast cash flow forecast in under 30 minutes. If I needed to, I could give this to my bank manager with confidence.

Total Time: 28 minutes

Review, Revise and Improve

So, I’ve just demonstrated how to prepare a cash flow forecast in under 30 minutes. To repeat this set of reports regularly, set up a workflow to deliver it to yourself and your accountant early each month. Once you have the setup, each month you will spend even less time.

Then, for the best outcome, schedule a chat with your advisor to discuss what’s happening with your cash flow and what problems the reports may reveal. By being proactive, you’ll help your business survive and set the scene for it to flourish and grow.

As time goes on, enhance your forecast by considering multiple future scenarios and be well-prepared for any eventuality.

Watch this short video tip on how to create a Quick 3-Way Forecast.